Invoice Factoring: How Small Businesses Improve Cash Flow Fast

Table of Contents

- What Is Invoice Factoring?

- Send Invoices in Seconds

- How Does Invoice Factoring Work?

- When Should Your Company Use Factoring?

- Pros and Cons of Invoice Factoring

- What Are the Different Types of Factoring?

- Invoice Factoring vs. Invoice Financing

- Reduce Dependence on Factoring With Strong Invoicing

- Ready to Strengthen Your Cash Flow?

- Send Invoices in Seconds

- FAQs

Invoice factoring is a financial transaction that allows a business to sell its unpaid customer invoices to a third-party factoring company in exchange for immediate cash—usually 70% to 90% of the invoice amount upfront. Instead of waiting 30, 60, or even 90 days for customers to pay, companies use invoice factoring to stabilize cash flow, cover operating expenses, and continue growing without taking on traditional debt.

Read our guide to understand what invoice factoring is and how it works, pros and cons of factoring agreements, and when invoice factoring for small businesses makes sense.

What Is Invoice Factoring?

Invoice factoring is the sale of accounts receivable to a factoring company at a discount. Instead of borrowing money, you convert unpaid invoices into immediate working capital.

This distinction matters:

- A loan creates debt and repayment obligations.

- Factoring is the sale of an asset (your receivable).

Under IRS guidance on factoring of receivables, a properly structured factoring agreement transfers collection rights to the factor and defines risk, fees, and settlement terms. Understanding this structure protects you legally and financially.

Invoice factoring is most common in industries with long payment cycles, including:

- Construction invoice factoring

- Freight invoice factoring

- Trucking invoice factoring

- Staffing and manufacturing

Before considering factoring, make sure your billing process is solid. Understanding invoices ensures your documents are legally clear and properly structured. Clear invoices reduce disputes and improve approval speed.

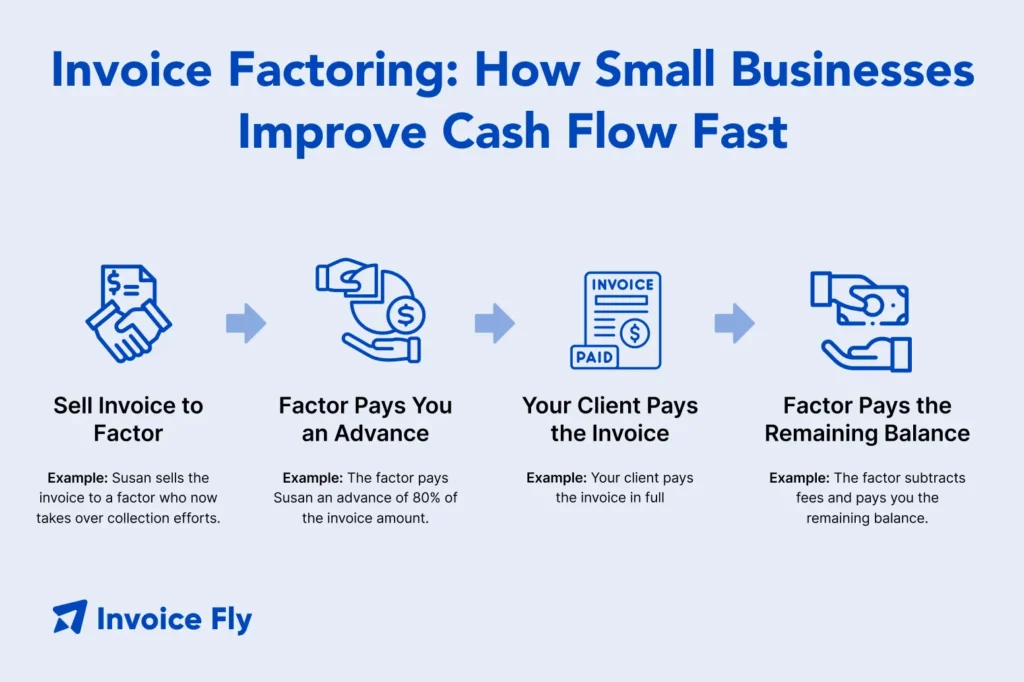

How Does Invoice Factoring Work?

The factoring process follows a predictable sequence. Understanding each step helps you evaluate invoice factoring companies confidently.

Step-by-Step Factoring Process

| Step | What Happens | Why It Matters |

| Invoice Issued | You complete work and send an invoice to your customer. | Clear billing reduces disputes. |

| Invoice Sold | You sell the unpaid invoice to a factoring company. | Transfers collection rights. |

| Advance Paid | You receive 70%–90% of the invoice amount. | Immediate cash improves liquidity. |

| Customer Pays | Your customer pays the factoring company directly. | Closes the receivable. |

| Final Settlement | You receive the remaining balance minus fees. | Determines true factoring cost. |

Clear invoice payment terms such as Net 30 or Net 60 directly influence how quickly factoring companies approve invoices. Understanding net 30 vs net 60 payment terms helps you assess how long your capital is tied up.

How Much Does Invoice Factoring Cost?

Invoice factoring costs vary by industry, volume, and customer reliability.

Common Invoice Factoring Fees

| Fee Type | Typical Range | Impact on Profit |

| Discount Fee | 1.5%–5% | Primary factoring cost |

| Service Fee | 0.5%–2.5% | Administrative expense |

| Wire/Admin Fees | Variable | Reduces final payout |

The total cost of invoice factoring depends on:

- Invoice amount

- Customer creditworthiness

- Industry risk

- Recourse vs non-recourse terms

Low-margin businesses should calculate carefully. Use the cash flow formula to measure how factoring fees affect your operating margin.

Invoice Factoring Example

Assume you issue a $100,000 invoice on Net 60 terms.

- Advance rate: 85%

- Immediate cash received: $85,000

- Factoring fee: 3% ($3,000)

- Remaining reserve after payment: $12,000

When your customer pays, you receive the remaining reserve minus fees.

Factoring Example Breakdown

| Invoice Amount | Advance (85%) | Fee (3%) | Final Payout |

| $100,000 | $85,000 | $3,000 | $12,000 |

This allows you to cover payroll, supplier payments, or marketing immediately instead of waiting two months.

When Should Your Company Use Factoring?

Invoice factoring for small business makes sense when:

- You have reliable customers but long payment terms

- Growth outpaces available cash

- You need short-term working capital

- Traditional loans are unavailable

Before entering a factoring agreement, evaluate whether improving your billing process could reduce delays.

For example:

- Set clear invoice due dates to prevent confusion

- Add structured invoice late fees to encourage timely payment

- Send invoices immediately based on best practices

Pros and Cons of Invoice Factoring

Invoice factoring can stabilize cash flow quickly, but it comes at a cost. Understanding both the financial and operational impact helps you decide whether it fits your business model.

Benefits of Invoice Factoring

Invoice factoring provides immediate liquidity and can support growth when cash flow is tight.

- Immediate access to working capital: You receive 70%–90% of the invoice value within days, helping cover payroll, materials, fuel, or marketing expenses without waiting for customers to pay.

- No new debt on the balance sheet: Factoring is the sale of a receivable, not a loan. This means you are not adding long-term debt or affecting traditional loan ratios.

- Outsourced collections: The factoring company manages payment follow-up, reducing administrative workload and freeing your team to focus on operations.

- Flexible funding tied to sales volume: As your invoice volume increases, available funding increases. This makes factoring scalable for fast-growing businesses.

- Easier approval than traditional loans: Factoring companies evaluate your customers’ creditworthiness rather than your business credit score, which can help newer companies access funding.

Drawbacks of Invoice Factoring

Factoring provides speed, but it is not inexpensive.

- Higher costs than bank loans: Invoice factoring rates and fees often exceed traditional loan interest rates, especially for higher-risk industries.

- Customer awareness of third-party collections: Clients are notified that payment should be sent to the factoring company, which may affect perception if not communicated clearly.

- Contract commitments: Some factoring agreements require minimum invoice volumes or long-term commitments.

- Less control over client relationships: The factoring company handles collections. If their approach is aggressive, it can strain customer relationships.

- Reduced profit margins: Factoring fees directly reduce invoice revenue, which may not be sustainable for low-margin businesses.

Invoice Factoring Pros vs. Cons at a Glance

| Advantages | Business Impact | Disadvantages | Business Risk |

| Immediate cash flow | Covers operating expenses quickly | Higher fees | Reduces overall profit |

| No traditional debt | Preserves borrowing capacity | Contract obligations | Limits flexibility |

| Outsourced collections | Saves administrative time | Customer awareness | Possible relationship strain |

| Scalable funding | Grows with sales volume | Less control over payment process | Reputation risk |

| Easier qualification | Useful for newer businesses | Ongoing dependence | May delay long-term financial stability |

What to Review Before Signing a Factoring Agreement

Before choosing invoice factoring services, review:

- Minimum monthly volume requirements

- Term length of the contract

- Termination clauses or penalties

- Recourse vs non-recourse terms

- All invoice factoring fees and administrative charges

Even small percentage differences in factoring rates can significantly affect profitability over time. Always calculate the full cost of invoice factoring against your gross margin before committing.

What Are the Different Types of Factoring?

Recourse Factoring

You are responsible if the customer fails to pay.

Non-Recourse Factoring

The factoring company absorbs bad debt risk.

Industry-Specific Factoring

Choosing the right invoice factoring company depends on industry specialization and fee transparency.

| Industry | Why Factoring Is Common |

| Construction | Long project billing cycles |

| Freight & Trucking | Net 30–60 payment norms |

| Staffing | Weekly payroll demands |

| Manufacturing | Large invoice values |

Invoice Factoring vs. Invoice Financing

These terms are often confused. Before choosing either, ensure your invoices are professionally structured.

| Invoice Factoring | Invoice Financing |

| Sell invoice | Borrow against invoice |

| Factor collects payment | Business collects payment |

| No debt recorded | Creates debt obligation |

| Higher fees | Lower interest (typically) |

Reduce Dependence on Factoring With Strong Invoicing

Invoice factoring solves short-term liquidity gaps. However, consistent billing practices reduce reliance on factoring over time.

Practical steps include:

- Use detailed line items to prevent disputes

- Include clear invoice terms and conditions

- Choose the correct types of invoices for recurring or milestone billing

- Track all invoicing payments to monitor aging receivables

Ready to Strengthen Your Cash Flow?

Invoice factoring can provide fast working capital when customer payments are delayed. However, long-term financial stability depends on consistent billing, clear payment terms, and real-time receivables tracking.

If you want better visibility into outstanding invoices and faster payment processing, using professional invoicing software helps you manage cash flow proactively and reduce dependence on costly factoring agreements.