What Is Invoice Financing And How Does It Work?

Table of Contents

Invoice financing is a funding method businesses use to access cash tied up in unpaid invoices. If you’ve ever finished a job, sent the invoice, and then waited weeks (or months) to get paid, you know how frustrating that gap can be. Invoice financing helps bridge that gap by giving you access to money you’ve already earned.

Instead of waiting 30, 60, or even 90 days for customers to pay, you can receive an advance — often up to 85–90% of the invoice value — from a lender. This form of accounts receivable financing helps keep cash flow steady, so you can cover expenses, pay your team, and keep growing. In this guide, we’ll explain how invoice financing works, which businesses benefit most, and how it compares to invoice factoring.

What is invoice financing?

Invoice financing is a short-term form of accounts receivable financing that allows businesses to access working capital by borrowing against unpaid B2B invoices.

It is a way for businesses to access working capital by using unpaid invoices as collateral. Rather than waiting for clients to pay on their schedule, you receive an immediate advance on what you’re already owed.

The lender provides a percentage of the invoice value upfront — typically 85–90% — and holds the remainder as a reserve. When your customer pays the invoice, the lender releases the reserve balance minus their fees. You stay in control of collections, and in many cases, your customers never know financing is involved.

To understand why this matters, it helps to know what an invoice is and how it functions as a formal request for payment. Every unpaid invoice represents real money your business has earned but hasn’t yet received — and invoice financing turns that gap into an opportunity rather than a liability.

The SBA identifies invoice financing as one of the primary ways small businesses can access working capital, particularly when traditional loans aren’t the right fit.

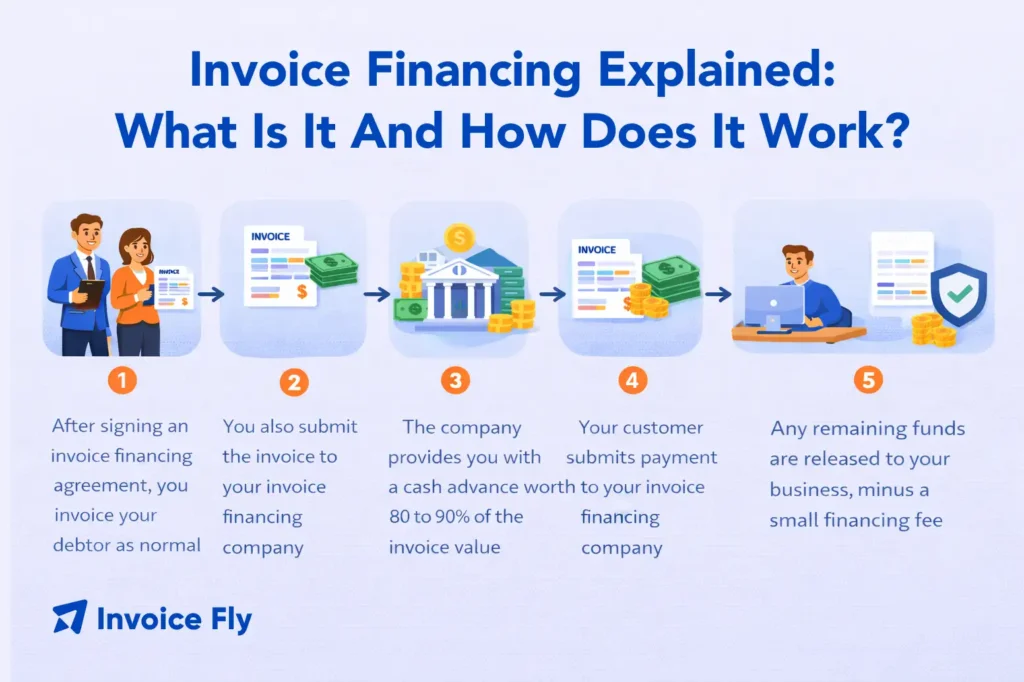

How invoice financing works

Businesses typically access invoice financing through banks, online lenders, or specialty invoice financing companies. The process itself is straightforward and follows a clear sequence:

- Issue the invoice. You complete work or deliver goods and send an invoice to your client with agreed payment terms.

- Submit the invoice. You submit that invoice to your financing company for review.

- Receive the advance. The lender advances you a percentage of the invoice total — usually 85–90% — often within one to three business days.

- Customer pays. Your client pays the invoice according to your agreed terms, either directly to you or to the lender depending on your arrangement.

- Lender releases the reserve. Once payment is collected, the lender deducts their fees and releases the remaining reserve balance to you.

Fees typically range from 1–5% of the invoice value, depending on the lender, the invoice amount, and how long the invoice takes to be paid. The longer it takes your customer to pay, the higher the total cost may be.

How to qualify for invoice financing

Qualification requirements vary by lender, but most invoice financing companies focus primarily on the creditworthiness of your clients rather than your own credit history. Key requirements typically include:

- B2B (business-to-business) transactions, not consumer invoices

- Completed work or delivered goods — lenders won’t finance invoices for work not yet done

- Clients with a reliable payment history

- Invoices that are not already past due or in dispute

Because the lender’s repayment depends on your client paying, your client’s financial reliability carries significant weight in the approval decision.

How to apply for invoice financing

Applying is generally faster than a traditional bank loan. Most lenders require you to submit your outstanding invoices, basic business financial information, and details about your clients. Many platforms offer online applications with decisions in days rather than weeks.

Before applying, it’s worth reviewing your invoice payment terms and making sure your invoices include all the professional invoice elements lenders expect to see — clear line items, payment due dates, and accurate vendor and client information. A well-structured invoice builds lender confidence and speeds up the process.

Structuring options for invoice financing

Invoice financing typically comes in three structures:

- Invoice discounting: You receive an advance on specific invoices while retaining full control of collections. Your clients pay you directly, and you repay the lender once funds arrive.

- Revolving line of credit: You draw against your accounts receivable as a whole, giving you flexible, ongoing access to funds as new invoices come in.

- Spot financing: You fund individual invoices on a case-by-case basis rather than committing to an ongoing arrangement — useful if you only need occasional access to capital.

Which businesses benefit the most from invoice financing?

Invoice financing is most valuable for businesses that issue invoices to other businesses and regularly experience gaps between delivering work and receiving payment. Common examples include staffing agencies, logistics companies, marketing and creative agencies, manufacturers, and B2B service providers of all kinds.

It’s particularly useful if your business is growing faster than your cash flow can support. When you’re taking on larger projects or more clients, your expenses often increase before your receivables catch up. Invoice financing bridges that gap and keeps operations moving.

Freelancers and small business owners who work with slow-paying enterprise clients can also benefit. If you’re issuing invoices with Net 30, Net 60, or Net 15 terms and finding it difficult to cover costs in the meantime, invoice financing offers a practical solution without taking on traditional debt.

Benefits and Risks of Invoice Financing for Businesses

Invoice financing has clear advantages, but it’s not without trade-offs. Understanding both sides helps you decide whether it fits your situation.

| Benefits | Risks |

| Faster access to cash — Get funds within days instead of waiting for slow-paying clients. | Cost can add up — Fees of 1–5% per invoice can become expensive over time. |

| No additional collateral required — The invoice itself serves as collateral. | You remain liable for repayment — If your client doesn’t pay, you still owe the lender. This is different from invoice factoring, where the factoring company typically assumes the collection risk. |

| Preserves client relationships — You typically manage collections, so clients may never know financing is involved. | Limited to B2B invoices — Not suitable for businesses working primarily with consumers. |

| Scales with your business — More invoices mean more potential access to funding. | Dependent on customer creditworthiness — Approval often hinges on your clients’ ability to pay. |

Invoice financing vs. invoice factoring

Invoice financing and invoice factoring are closely related but work differently in a key way.

With invoice financing, you borrow against your invoices. The invoices serve as collateral, you retain ownership, and you are responsible for collecting payment from your client. You also remain responsible for repaying the lender even if your client doesn’t pay.

With invoice factoring, you sell your invoices outright to a factoring company at a discount. The factoring company takes over collections and assumes the risk of non-payment. Your client pays the factoring company directly, and you have no obligation to repay if the client defaults.Invoice factoring is often simpler but more visible to your clients. Invoice financing gives you more control and confidentiality but keeps the repayment risk on your side. Knowing how to write an invoice correctly and how to avoid common invoicing mistakes becomes even more important when financing is involved, since invoice quality and invoice due dates directly affect your access to funds.